RISK WEIGHTING

A first visit to a wealth manager will usually result in the offer of a menu of “risk weighted” portfolios which are intended to deliver a return appropriate to the investor’s risk appetite. The more cautious, the lower the risk – and the lower the anticipated return. This meets the regulator’s requirements and has a veneer of intellectual credibility.

The standard menu is based around a mix of bonds and equities. The higher the investor’s declared risk appetite, the higher the equity weighting, and the more likely that the equities component will be supplemented by exposure to hedge funds or structured products.

This sort of approach goes back to the 1950s when Harry Markowitz, inventor of the Modern Portfolio Theory (for which he was awarded a Nobel Prize), showed that holding a mix of unrelated assets that do not behave in the same way will significantly reduce risk (that is to say the variance of returns) in portfolios. He suggested that a 60:40 mix of equities and bonds would be the optimum mix of assets, though this was not part of the theory per se. At more or less the same time in the UK the “cult of the equity” emerged among UK pension fund managers taking the view that the best way of capturing the long term growth of the economy was through equity ownership.

The 60:40 approach relies on bonds being less volatile than stocks and economic growth and inflation moving up and down in tandem. Simplistically, with economic growth equities should rally but inflation is also pushed up bringing returns down on bonds, and likewise in recession equities will underperform but with inflation low and interest rates coming down, bond prices will be pushed up.

The strategy has for decades provided investors with relatively safe returns. However, with the onset of the pandemic the link between economic growth, inflation and interest rates was disrupted, with central banks aggressively cutting rates and governments increasing spending dramatically. In the post-pandemic normalization, bonds suffered as rates went up, and the longer the duration of the bonds (or more usually the bond funds) the worse they suffered. Moreover, supposedly low risk portfolios destroyed value – a 60:40 fund in the US would have underperformed inflation by c. 30% in 2022.

THINKING ABOUT LIABILITIES

An investor making independent decisions needs to put some more thought into the process when deciding on their asset allocation. One important consideration may be to think about investing assets in ways that match future liabilities and offset risks:

Retirement income:

- This is the most obvious. In order to achieve a core level of income and certainty, a laddered portfolio of bonds makes a lot of sense, with maturities spread over time. This could incorporate index-linked bonds to offset inflation risk. As interest rates have returned to what are, by historical standards, more normal levels, annuities have started to look more attractive too, though they do provide the certainty of loss of capital at the end of life.

Providing against future school or university costs:

- Again, bonds with maturities at the time of the planned outflow are a useful organisational device. This is particularly due to the availability of Gilts and other sterling bonds trading on a discount to their maturity value, which under the Qualifying Corporate Bond (QCB) Exemption offer part of their return (from the purchase price to the redemption value) tax free.

Providing for overseas retirement:

- Providing for overseas retirement (as well as potentially offering the chance of escaping UK inheritance tax) should logically be offset with assets in the intended destination – Euros or US dollars as a proxy against more distant destinations.

Inheritance Tax liabilities: (Please note that this is not tax advice).

- Whether we will see a market develop in £1m – worth packages of agricultural land with tenancies attached – taking advantage of the likely sales of family farms precipitated by the latest budget – remains to be seen. For now, the biggest exemptions are the seven year (perhaps to increase to ten years) survival requirement for potentially exempt transfers (“PETs”) and the currently uncapped “normal expenditure out of income” provision.

- Term Insurance written in trust to the beneficiary is an interesting option for those making PETs.

- Demonstrating to HMRC that regular payments are out of surplus income may be facilitated by tying payments to specific income streams – e.g. from bonds. HMRC’s internal guidance on this can be seen here.

NEW TRENDS

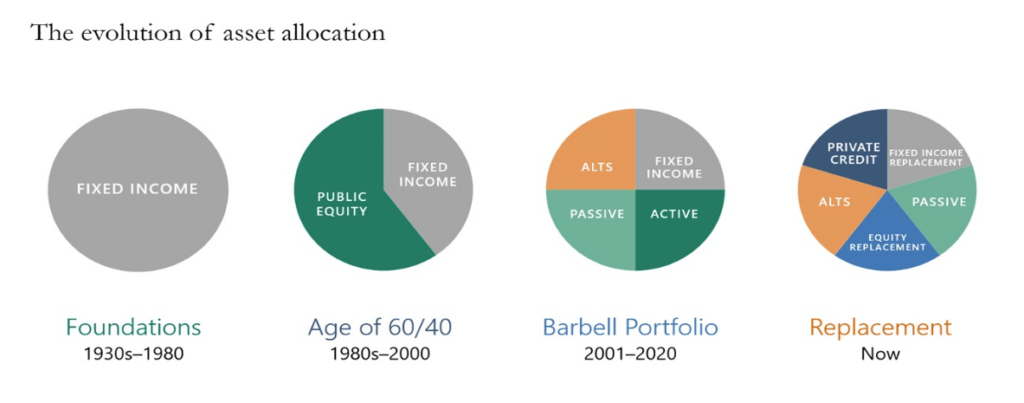

More recently we have seen some creative attempts to define what a healthy mix of assets ought to be, to some extent reflecting the increased range of investments available to investors. As an example, the US asset manager Apollo Global Management recently published a graphical history of the development of asset allocation (for a US audience) from an all-bond portfolio to a mix of asset types:

Source: Apollo Academy

Source: Apollo AcademySome of the categories are of questionable relevance to private investors. By way of explanation:

Alternatives – this includes derivatives and structured products, as well as hedge funds and commodity funds.

- Simpler structured products can be very useful to private investors who may be willing to sacrifice some of the upwards potential in portfolios for some downside protection. There are traps for the unwary, and embedded fees can be an issue.

Active implies either actively managed equity funds or direct investments in equities.

- This is, of course, well-trodden territory for private investors.

And correspondingly “passive” implies indexed funds, whether structured conventionally – as unit trusts or other mutual funds, or as Exchange Traded Funds (ETFs) which have the advantage of instant liquidity.

- We shall return to the active vs passive question in a future article.

Fixed Income Replacement and Equity Replacement is a nascent trend in the US for larger funds to invest in untraded bonds (not such a radical step given that the liquidity in bond markets outside of government bonds tends to be quite limited) and in private equity – with or without the without the financial leverage that private equity funds employ.

- This is not directly relevant to private investors, at least in the UK.

Lastly – and this is now a global trend – we are seeing increasing direct lending by institutions, disintermediating the banking system. As the banks have shut branches, reduced the range of lending they provide, and reduced direct contact with borrowers, they have created an opportunity for alternative lenders (and leasing and financing companies) to offer faster and more flexible funding.

- Whilst this is not practicable for private investors, LGB’s MTN programmes are an efficient way for investors to get exposure to alternative finance companies themselves.

PROPERTY

Apollo does not mention real estate – presumably this is not unconnected with their not managing property funds. In the UK (but not in the USA where property funds are invariably private) there is a wide range of quoted property investment vehicles, and private investors historically have invested also in rental property, and for different reasons (IHT, and CGT rollover relief) in farmland. The problem with property is that it cannot be moved. Which makes it particularly vulnerable to tax hungry Chancellors – and so it is now proving. It is probably easiest to access property through quoted funds – or through MTNs with exposure to property lending.

STRUCTURED PRODUCTS

Structured products, using derivatives to provide customized outcomes, can be thought of as insurance products- and like insurance the embedded costs need to be born in mind. It is possible to hedge against adverse outcomes by giving up a certain amount of upside. It is also possible to take what are in effect bets on outcomes. These can be shark-infested waters but by focussing on the risk management products investors can make effective use of them. At LGB we have been engaging with some of the providers and may from time to time offer suggestions of strategies employing them.

CONCLUSION

There is no right answer to the question of how to allocate assets. But we would urge you to:

- Stay within your comfort zone.

- Think hard about your objectives and requirements.

- Use fixed income securities to match foreseeable outgoings.

- The risk of changing interest rates can be managed through laddered bond portfolios.

- And don’t put all your eggs in one basket.