Market Commentary: The Known Unknown… and the Known Knowns

The Known Unknown for 2025 is the second iteration of a Trump presidency. It casts its shadow very broadly and there has been much reading of the runes trying to work out how much of what he said last time he was in the White House was actually put into place. And to what effect. The Fed has been downplaying the effect of tariffs on inflation (it is interesting that the anti-China rhetoric and tariffs of the first presidency were a period when the S&P China 500, the Chinese index in US$, rose 80%). The market is less confident.

The Known Knowns are what happened last year. We will start with the bond markets which generally lead the equity markets for two reasons. First, many analysts use bond yields to determine the present value of future earnings and dividends. Secondly, fund managers and even private investors make allocations between bonds and equities that have an effect on the relative performances of both markets.

Fixed Income

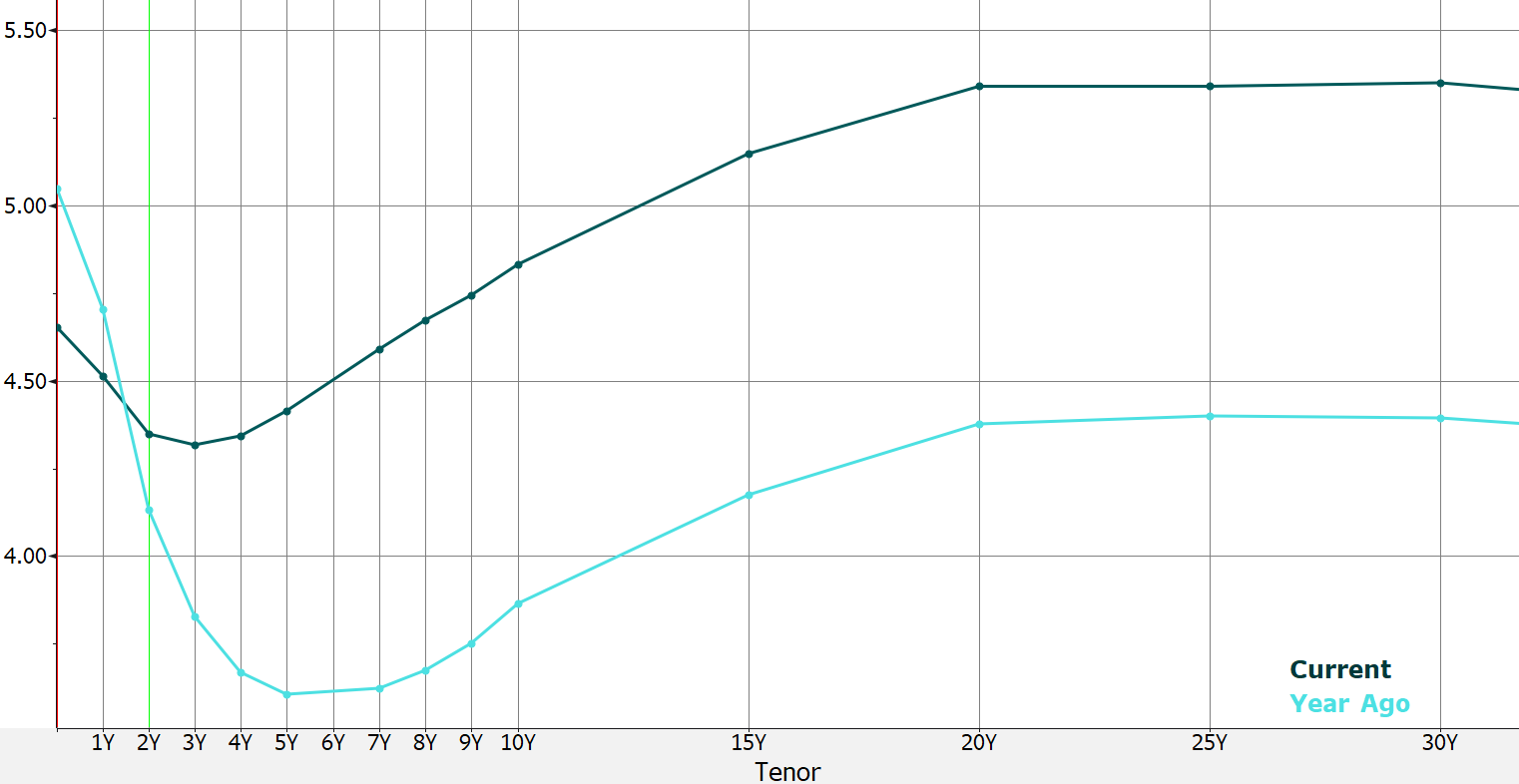

Looking back a year, we were faced with so-called inverted yield curves across all the major bond markets, implying falling rates on the back of falling inflationary expectations.

Instead, inflation has proved stubborn and government borrowing requirements high. The bond markets are not being generous to them. At the time of writing, the UK 10 year gilt is trading at a yield to maturity of 4.9% vs around 3.8% a year ago, the highest rate since 2008. This compares with one month sterling T-Bills yielding 4.7% vs 5.2%. If you are willing to lend your money to HM Treasury for 30 years, you will be paid over 5.4% vs under 4.5% a year ago- as the media has spotted, the highest rate since 1998. Index Linked Gilts have also weakened- the 30 year auction on 14 January offered the highest after-inflation yield since 2006, offering almost 2.13% (so implying that the market anticipates inflation of over 3% for the next three decades), not a great expression of confidence in the MPC.

In the US, ten year rates which were around 4.1% a year ago are now at 4.7%, and at the longest end of the Treasury yield curve (30 years) rates are at almost 5%. Four week US T-Bills yield 4.3% vs 5.4%.

Even German rates have risen – 10 Year bonds now yield 2.5% vs 2.2%, and the Euro market is showing some quite wide disparities: French 10 year rates for example are at 3.3%.

An environment in which yields are trending higher presents risks and opportunities to investors depending on how they are making fixed income investments. The risks are associated with investments in bond funds, usually with medium term durations, typically of five years. A one percent increase in yields will result in a 5% fall in the NAV of such a fund (and of course vice versa if yields fall). In contrast investors with a laddered portfolio of bonds and a ‘buy-and-hold’ strategy can reinvest interest payments and redemptions at the higher yields and increase the return from their portfolios. They will not suffer a capital loss if they hold their bonds to maturity.

Equities

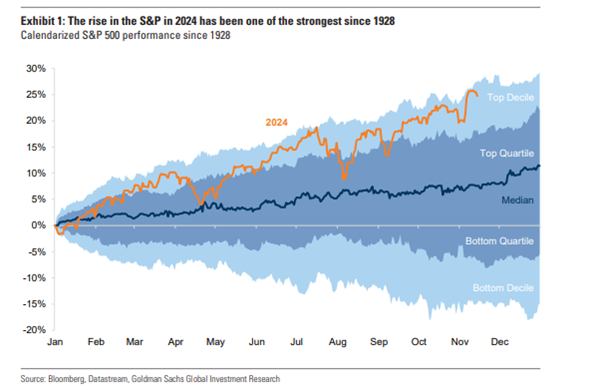

Given the strength of the US equity markets and the current level of bond yields, questions are being asked as to whether equity prices in the US are too high. The rise in US equity markets last year was one of the highest in the last century, half driven by earnings and half by valuation expansion:

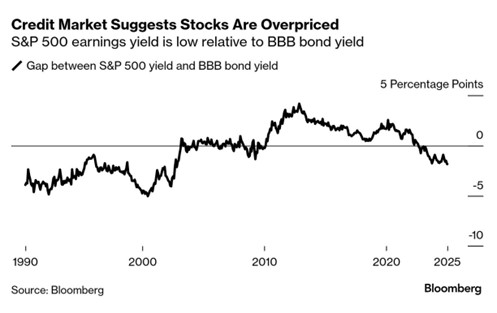

And given that one explanation for valuation expansion is that there was optimism about lower inflation and interest rates, this must at least give some grounds for concern. See for example this Bloomberg chart comparing the so-called earnings yield (the reciprocal of the price earnings ratio) against the yield on BB -rated US corporate bonds:

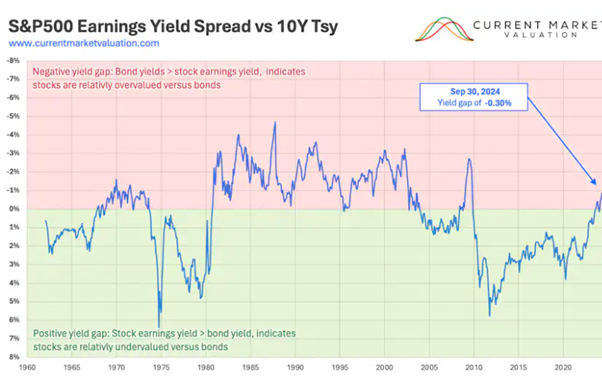

But it rather depends at which period you look at- and arguably the period of super-depressed bond rates due to Quantitative Easing was the exception. Looking even further back (and comparing against Treasury yields) the norm was for equities to look expensive:

This sort of measurement tends to be broad-brush. US equity valuations remain distorted by the weighting of the Magnificent Seven tech stocks (PE ratios around 40x vs 20x for the rest of the market). Beneath that valuations are more modest, and the economic and earnings growth anticipated in the USA remains higher than elsewhere in the world. Falls in the market tend to come due to or in anticipation of recessions which is not the expectation in the USA. Elsewhere in the world, in the UK particularly, equities are not expensive. But the economic outlook is less encouraging.

What Might Change in the UK?

The initial business enthusiasm for the new brooms in numbers 10 and 11 Downing Street has evaporated. In contrast to the robust “animal spirits” of the USA, confidence has been damaged by NI increases, borrowing cost increases, and what feels like generally an adverse investment climate. The Prime Minister’s preference for improving ties with the EU may militate against doing deals with the US and carry dangers of being more tangled than necessary in a tariff dispute. Pressure to increase defence spending (something we shall write on separately) at the same time as delivering on promised increases in public services (which should see some beneficiaries amongst service suppliers to the NHS) seems to point to higher taxes. What might give is that the Bank of England decides – as it did through the QE period – that its inflation target is less important than the overall health of the economy and forces rates down. If that were to happen, locking in the interest rates currently available in the Gilts market would seem like a smart move. But it would be a significant policy change and the circumstances in which it happens might look quite ugly.

The UK equity market is continuing to see companies migrating to the USA as well as takeover activity, in large part from outside the UK, in part in-market consolidation. Only a little of this is slipping into the AIM market, which fell 9% last year vs the FTSE All-Share index which rose 5.5%. The structural problems of AIM- in particular a lack of dedicated institutional investors, and an absence of new funding for those that do exist – shows no sign of abating.

It is worth noting that the energy transition which was a very current topic a year ago is now unlikely to be a market driver as the cost of net zero is becoming an increasing concern and the Trump administration seems to have little interest in it, which could have an impact on the whole sector.

A few commentators have argued that tax sheltered investment in ISAs, SIPPS and pension schemes should be directed towards the UK- why should an ISA investment in Tesla be tax free? However, there seems little official support for this. The government killed off the “Brit ISA” plan and its intention to group together public sector pension funds seems to revolve around encouraging more infrastructure funding from them – it will in any case take some years before anything comes of this.

Opportunities

There will be an opportunity to lock in high interest rates in the UK and possibly elsewhere in Europe through the buying of longer duration bonds, either as inflation fears subside, or as relevant central banks (particularly the Bank of England) move to avert damage to weakening economies and cut rates- but timing this will be tricky. The laddered fixed income portfolio continues to be a good strategy to avoid timing decisions and reduce the risk of interest rate surprises.

In equity markets, the perhaps-too-obvious sectors are a continuation of the strength in defence and high tech- the AI story is not going away though there will be as many or more losers as winners. Scanning the world, animal spirits in the US remain strong and supportive and it would be brave to bet against a continuation of its strength. A move by China to reflate its domestic economy if it can not rely so much on exporting may create interesting opportunities, with potential spillovers into resource shares involved in its supply chain (the major miners). The US equity market is the place if you do not fear the collateral damage that MAGA might cause.

Overall- a new Trump presidency will bring surprises, and problems for the rest of the world, and investors will need to be agile- short dated fixed income investments such as T-Bills remain a relatively safe refuge if you lack conviction.

In summary, a sensible approach seems to be to improve the quality of portfolios by increasing allocations to fixed income and shares of robust companies on attractive PE and yield valuations, while waiting for the surprises to create investment opportunities during the year.