This is the time of year when commentators go into peak pontification mode, and it would be a shame not to participate, particularly when so much has been going on in the world. So firstly a few general thoughts, and then some thoughts on interest rates and implications for UK bond investors.

The bigger picture

The election of Donald Trump has been the dominant concern for pontificators, but the collapse of the Assad regime will have consequences too, potentially over time (if oil and gas pipelines across Syria are reopened) reducing energy insecurity. In both cases we see as through a glass, darkly. However we can see some shapes. Ukraine seems to be less of a short-term concern, with tensions having been dialled down in the expectation that the new US administration will reduce support and oblige the Ukrainians to do a deal.

In the US it looks as if the Fed will approach the change of regime cautiously (even though the Fed policy will wait for government policy to actually change rather than to anticipate it): deregulation could support growth and dampen inflation overtime; tax cuts might boost demand quite quickly; raising tariffs would do the opposite, and could also be inflationary (though experience of Trump’s first administration was that a lot of the threatened tariffs were bargained away, and that Chinese exporters found effective ways of routing exports through third countries); and deporting working immigrants might have similar, and potentially larger, effects. But the extent to which all or any of this will actually happen remains uncertain. It is also unclear how much the new administration will directly try to influence Fed governance, albeit that would be legally challenging. Interestingly the threat of US tariffs seems to have contributed to a policy response in China, which by embarking on a domestic stimulus programme will increase domestic consumption of its surplus output.

The effect on the dollar is a further imponderable. It was broadly unchanged by the end of the first Trump term. Whilst higher inflation and higher interest rates would support a stronger dollar, it is already relatively strong by recent standards.

Thoughts on interest rates

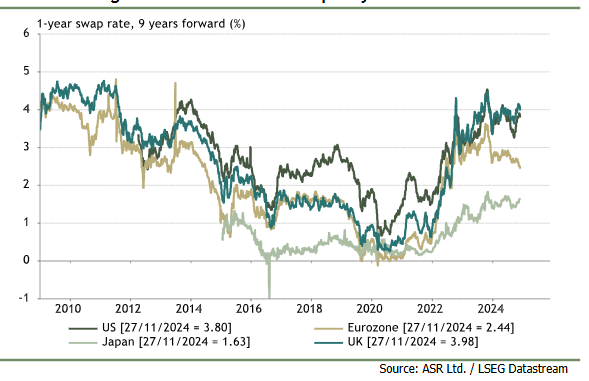

So far as forward rates are a prediction, the market is now expecting US rates to stay higher for longer, and other measures give similar results: Absolute Strategy Research have plotted long-run forward rates as a proxy for what the central banks might consider to be a neutral or Goldilocks rate, and concluded that the room for further rate cuts was modest, with the UK Bank Rate and US Federal Funds Rate converging around 4%. As for where we are today, the latest (13 December) T-Bill auction came in with average interest rates of 4.71% for 1 month and 3 month and 4.66% for six-month maturities. This compares with the equivalent US bills returning 4.29%, 4.34% and 4.31%.

ASR have also plotted 10-year Treasury yields against nominal GDP growth and the Fed Funds rate and suggest that equilibrium 10-year yields could be as high as 5% (currently about 4.24%):

In the UK, more than a month has passed since Rachel Reeves’ first budget. Unlike in the US, the new administration seems to have done its best to mute animal spirits, and the Growth Agenda is hard to locate. The budget did imply an increase in growth projections – from government spending – but the collateral damage to business confidence from national insurance contributions and otherwise, as well as from higher interest rates, is not at all encouraging. Whilst the move towards netting off government investment against borrowing is logical, it does not disguise that overall borrowing expectations have risen (and will ratchet up even further given rates are higher than the OBR had projected) and the Gilts market is exacting a price for funding that increase.

Implications for UK Bond Investors

UK inflation is variously expected to remain between 2-3% over the next few years, so above the Bank’s 2% target. The OBR forecast for example is for RPI and RPIX (excluding mortgage payments) both to drop to around 2% next year but to settle around 3% by 2027-2028. The Bank’s track record in tackling inflation has been unimpressive over the last few years, persisting with Quantitative Easing long after the rationale had passed. Let’s therefore take 2.5% as a working assumption (+/- 4% Bank Rates make sense in this context). That is then our hurdle for retaining the value of savings.

In so far as bonds are held within tax wrappers, ISAs particularly, current yields will do the trick. UK 10 year Gilts currently yield c. 4.3%, towards the higher end of the year’s range, you would have to go back to before 2008 to find them yield consistently more than this. For investors who are looking to buy or have bought Gilts and other Qualifying Corporate Bonds which are exempt from capital gains tax (see the HMRC guidance) at a discount to par (usually if they have very low coupons) a large proportion of the return will be tax free. Take for example the 0.625% Gilt maturing 31/07/2035, currently priced around 69.04. Only the 0.625% annual coupon will be subject to income tax. The capital gain over 10.5 years will under current rules be untaxed. Therefore the return to a 45% tax payer would be about 4% net, so around a 1.5% real annual return if our assumption of 2.5% inflation is correct. This assumes a buy-and-hold strategy, and investors should be aware that a long-dated bond will be more sensitive to changes in interest rate assumptions which will affect its mark-to-market price during the holding period.

Our weekly bond list, available on the LGB Deal Hub, highlights several corporate bonds in GBP trading at a discount to par. For instance, the KFW 1.25% 31/07/2026 bond is trading at 95.8, offering a pre-tax yield of 4.42%, while the Goldman Sachs 1.5% 07/12/2027 bond is priced at 91.18, with a yield of 4.69%.

Ultimately the bonds issued during the period of super-low rates will mature and the opportunity will disappear. But the opportunity is attractive while it lasts. Bonds held within funds do not provide this tax advantage. It is certainly a way of conserving wealth, providing that inflation does not spike up, or the value of sterling collapse (which would itself cause inflation to spike) or the UK government decides to stop paying its debts. If inflation is indeed reduced to 2% or less it starts looking much more attractive. Gilts do therefore have their place within a laddered portfolio, alongside a mix of maturities and credits. With a buy-and-hold strategy for a bond portfolio, there is certainty about the gross return, although inflation remains the uncertain factor.

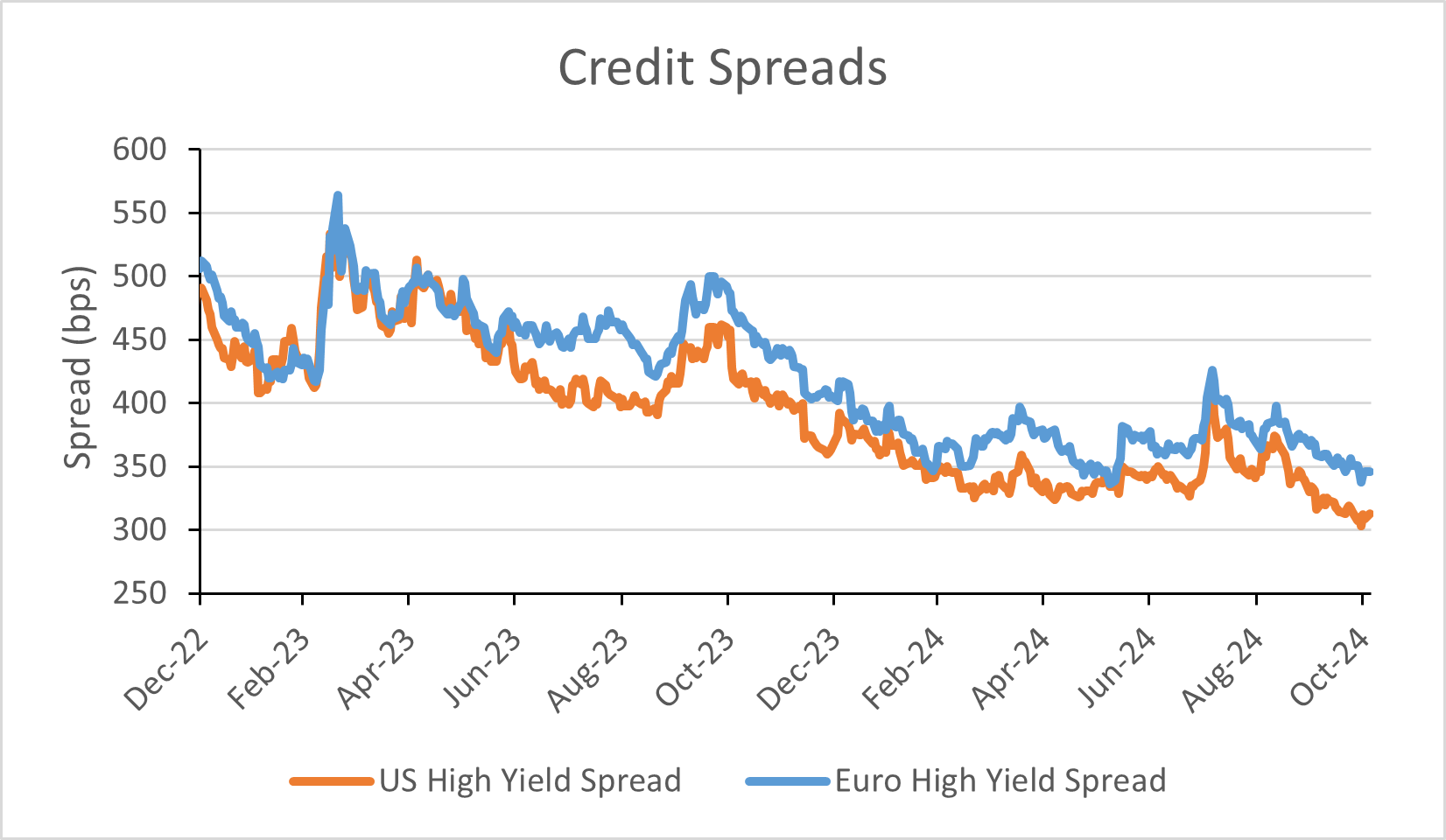

What about the higher return element of a laddered portfolio? There may be no free lunches but some lunches are unarguably more attractively priced than others: the idea that market prices in relative risk perfectly is not sustainable. The UK unlike the US does not have a particularly deep corporate bonds market available to private investors. In the US (and Europe) it is relatively easy to track the premium investors get for taking on the additional credit risk of corporate debt- and this premium over equivalent maturity government bonds (the credit spread) has been coming down as optimism for the economy increases:

The same has happened in the increasingly large private credit market, largely a US feature ($1.5tn in 2023, an estimated $2.6tn by 2029 according to the FT, other estimates are higher. The largest fund manager in the space, Apollo, is talking about having $1.5tn of assets in five years, which proponents suggest has a default rate of around 1.7% and average yields around 12%. LGB’s MTN issues fit in broad terms into the private market space, but for now rates remain high (8.75%-12% p.a.). Issuers continue to pay a premium in return for the flexibility offered by the MTN programme structures. Maturities are relatively short and in some cases duration is further reduced due to amortisation features. With LGB undertaking due diligence and monitoring, private investors are able to build diversified laddered portfolios at attractive average yields.

In January we are expecting new issues from Shire Leasing, Sema Lease and Simply Asset Finance though these are subject to change and terms are still to be confirmed.

Conclusion

Whilst investors will have their own views, we are inclined to think that rates stay higher for longer, and that there is no clear attraction in “extending the ladder”: a laddered portfolio with a mix of higher yielding shorter term MTNs and longer-term investment grade bonds and Gilts currently trading on discounts should provide an acceptable risk-return profile.