Aux Armes - Citoyens!

Not everyone is comfortable investing in defence companies. Over the years there are few that have not done businesses with regimes who either at the time or over time have looked unpalatable. Arms contracts have a history of being accompanied by payments to middlemen and direct bribery. At the most basic level, weapons are designed to kill people.

ESG criteria appear to lead to the exclusion of various defence stocks, and in 2023 the FT found that “investment funds had cut their holdings in Britain’s leading defence companies by an average of 9% since early 2022, with some citing ESG considerations”.

However, more recently, investor interest in the defence sector appears to have intensified. In 2024, the Asia-Pacific region witnessed the launch of 15 new defence industry-focused exchange-traded funds (ETFs), a significant rise from just one in 2023 (see here). The UK government has called on the financial services industry to step up its support for the UK’s defence companies. In the US, ESG investment is very definitely out of fashion already.

Times and perceptions change, and against a backdrop of new conflicts investors may judge that an allocation to the sector makes sense within the context of their investment portfolios.

Where are We Now?

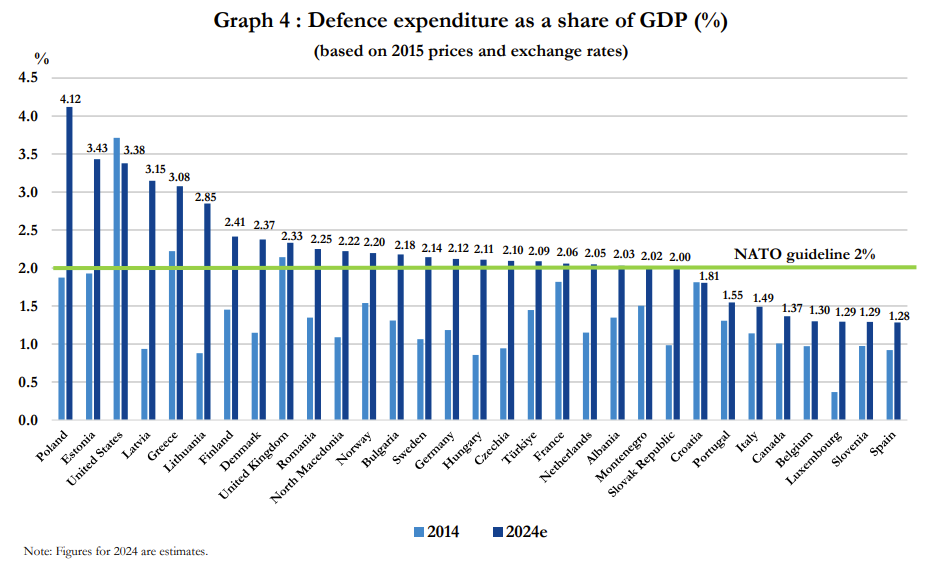

One of the achievements of Donald Trump’s first presidency was to persuade NATO members to start to increase their defence spending towards the 2% target that they had agreed in 2006, which most had fallen below. This was before the Ukraine invasion, and before it became evident that China is now representing a real threat to US naval supremacy in the Pacific & South China Seas. Even now the USA spends 63% of the total NATO budget.

The new administration seems highly likely to come in with much higher targets. On 20 December the FT carried a story that “Donald Trump’s team has told European officials that the incoming US president will demand NATO member states increase defence spending to 5 per cent of GDP.” Iain Martin’s Reaction Substack carried a similar story – and qualified it with “Trump is going to demand 5% and settle for 3.5%.” The US itself spends a little under 3.5%.

The majority of NATO countries are currently spending over 2% on defence, with some conspicuous laggards and some real disparities in the effectiveness of that spending – Germany’s “Zeitenwende” has not yet even started to transform the country’s badly neglected armed forces, for example.

The scale of potential additional spending is striking. Deutsche Bank suggested in a recent report that: “Raising the NATO spending target from 2% to 3% is equivalent to an extra $180bn per annum of spending. If a 3% target is phased in by 2030, it would be equivalent to more than $600bn extra spending relative to the 2% target by the end of the decade.”

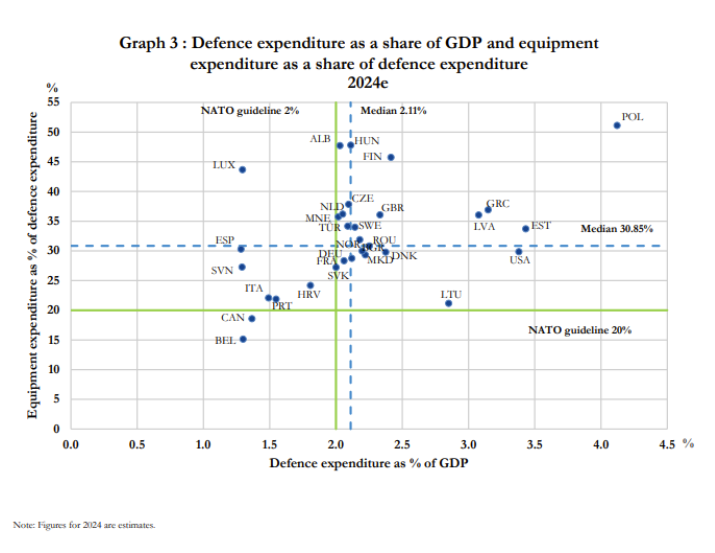

Bias to Equipment Expenditure

Moreover, increases in spending are likely to result in higher expenditure on materiel as a proportion of overall costs. The UK MoD for example in 2022-23 spent about 26% of its budget on staff, with 38% on capital equipment & R&D plus another 15% on equipment support. Poland, which is at the top of the chart below and which has been ramping up defence spending most quickly in NATO, has the highest proportion of spending on equipment. So even an overall increase in spending across NATO from 2% to 2.5% of GDP would logically lead to much more than a 25% increase in equipment expenditure:

We are already seeing this in the numbers. NATO estimated that equipment spending by its members ex the USA rose 36.9% in 2024 over 2023.

(Source- NATO)

Other Trump Effects

Donald Trump has also committed to ending the Ukraine conflict – presumably with a frozen front line. It will be little comfort to the Eastern European states which feature at the left-hand end of the first chart. Allowing Russia to continue its occupation would effectively have rewarded Putin’s invasion and given him confidence that – after a suitable pause to rearm – further adventures against neighbours will be practicable. And with China’s arms industry continuing to outbuild the USA, Europe will it seems increasingly be left to defend itself. Therefore, any temporary relief post a Ukraine deal is likely to be short-lived. And the consensus that a solution will be easy to find may be incorrect. Professor Laurence Freedman points out that Russia is suffering from war-weariness but also that President Putin is not interested in marginal territorial gains but in the extinction of Ukraine as an alternative to his kleptocracy.

There is some concern amongst the larger prime contractors in the USA that the new administration will favour new entrants to the industry and those close to the MAGA oligarchy. As the FT noted on 16 January (paywall) “industry executives and investors fear the Trump administration will disrupt the established defence hierarchy by giving lucrative contracts to newer players.” Since the US election, many of the established players such as RTX (Pratt & Whitney, Raytheon etc), Northrop Grumman, General Dynamics and Lockheed Martin have underperformed the S&P 500.

Defence Stocks vs The Wider Market

Defence stocks worldwide have been a major gainer over the three years since Ukraine was invaded. Performance has however been uneven, and many large defence contractors are also in civil aerospace – Boeing (still the second largest component of the Dow Jones US Aerospace and Defense index) and its supplier Spirit have had well documented problems in their civil aircraft businesses. The Dow Jones U.S. Select Aerospace & Defense Index has compounded at 12.4% per annum over the last three years vs 7.2% for the S&P500. An element of this outperformance may have been the unwinding of some of the ESG bias against defence companies in fund management. This has become politicised in the USA, less so in the UK.

It is important to consider that security threats increasingly include unconventional hostilities through cyberattacks and attacks on marine communications. Consequently cybersecurity, AI and data analytics companies very much come into the relevant universe. Peter Thiel’s AI pioneer Palantir is the largest component of some of the indices, selling to various parts of the US military, as well as to other governments and to contractors – it does also have a substantial non-defence business.

In the UK, BAE Systems has gained a mere 3.5% over the last 12 months, having roughly doubled in the previous two years since before the Ukraine invasion. In the same period Germany’s Rheinmetall has doubled in the last year, having previously trebled. UK defence spending has had a bias towards large projects such as the two aircraft carriers and the nuclear deterrent programme. The Ukraine war has demonstrated the need for volumes of conventional materiel, drones and manpower. It has exposed a gap in the UK’s defences against ballistic missile attacks.

Big Contract Problems

Large, multi-year contracts can and do go wrong. Governments can and do have budget issues and changes of priorities: the UK Defence Review has already hurt a number of smaller companies as programmes were deferred. Engineering challenges can cause costly problems to the contractors, and whilst they try hard (and often succeed) in transferring risk to government, it does not always work. Gearing up creates working capital issues and the profits from multi-year contracts tend to be back-end loaded which can sometimes encourage creative accounting to maintain market confidence in the early years.

Companies can invest in the anticipation of business that simply does not arrive. For example, winning the lead subcontractor position in the huge fleet solid support contract did not save Harland and Wolff (though re-pricing it will presumably set up the Spanish state-owned Navantia well), Chemring fell sharply after problems at a US factory, as did Solid State after a major defence contract was held up by the UK Strategic Defence Review.

How to Invest

There are a limited number of funds accessible to UK-based investors, and investors should note that there is no commonly agreed international (as opposed to US) index on which these ETFs are based. They are managed to replicate synthetic indices which the managers themselves specify, but are not actively managed. We have not located an actively managed defence fund accessible to UK private investors. Interestingly former Defence Secretary Sir Ben Wallace is now involved in a private equity fund investing in private defence companies.

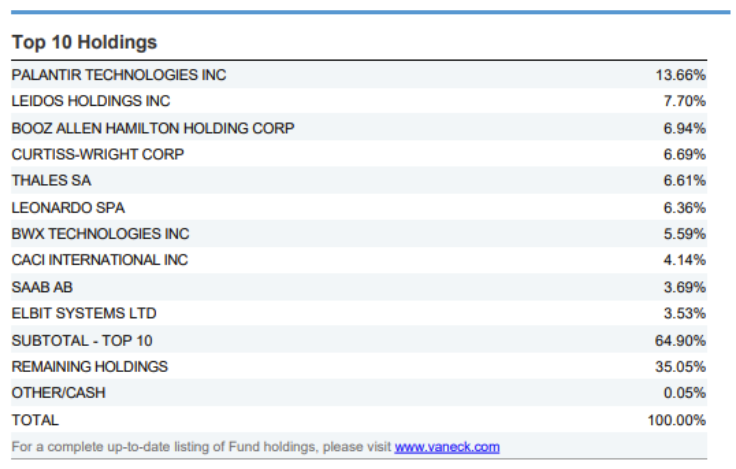

The VanEck Defence ETF, with assets of $1.9bn (the KIID is here) is about two thirds invested in the US, a little under a quarter in Europe and the rest in S. Korea, Israel and Singapore. Its largest holdings are the software company Palantir, Leidos Holdings (the merger of part of SAIC and Lockheed Martin), the management consultancy Booz Allen Hamilton Inc, which Bloomberg describes as “the world’s most profitable spy organisation”, Curtiss Wright (US- components), Thales (France) and Leonardo (Italy).

Source: VanEck

The $625m Future of Defence UCITS ETF “NATO” managed by HANetf also has Palantir as its largest holding, followed by Rheinmetall, Safran (France), Fortinet, Crowdstrike and BAE Systems. It tracks the EQM Future of Defence Index.

First Trust launched a Global Aerospace and Defence UCITS ETF in December 2024, intended to track the indxx Global Advanced Aerospace and Defence Index.

All the above ETFs are available for trading on the LGB Investments platform and can be held in ISAs. Investors preferring individual stocks can also contact us for further analysis.

On the assumption that international tensions stay high, that the increases in spending already planned but not yet delivered start feeding through to contractors’ P&Ls, and that the direction of travel is towards still greater spending, the defence sector may well be one to watch in 2025.

This article is not a financial promotion and is not intended as an offer or solicitation to enter into investment activity with any recipient of the email. Any opinions expressed are the opinions of the writer at the date of circulation and do not constitute investment, legal, tax or other advice. LGB has not independently verified the content of any third-party material referred to in this email and makes no representations as to the validity of any of them.